De-Risk Your Portfolio with Whole Life Insurance

Podcast: Play in new window | Download

In the quest for financial stability, a de-risked portfolio serves as the cornerstone of a secure future.

Whole life insurance is an often-overlooked instrument that plays a pivotal role in achieving this stability. By moving assets into a whole life insurance policy with accumulated cash value, you can transform your retirement savings into a resilient safety net. Not only does it provide life coverage, but it also offers a non-correlated asset that can grow over time and assist in mitigating market risks.

Employing a whole life insurance policy to supplement retirement income involves strategic use of policy loans, which can be advantageous due to the policy’s accumulated cash value.

If you elect to generate income via policy loans, understanding the implications of paying annual loan interest is paramount.

While the idea of taking on a loan in retirement might seem counterintuitive, the annual income potential from the policy, optimized by savvy handling of loan interest, can significantly exceed the interest payments, creating a beneficial financial situation.

Key Takeaways

-

- A whole life insurance policy serves as a dual-benefit financial tool, providing both security and growth.

- Policy loans from whole life insurance can amplify retirement income due to positive arbitrage between income and loan interest.

- Strategic management of a whole life policy and its loans maximizes financial success during retirement.

Life Insurance as a Stability Anchor

In the landscape of financial safety nets, life insurance stands as a stalwart hedge against market turbulence. Let’s examine how incorporating it into your grand investment scheme enhances stability.

-

-

- Guaranteed Protection: Traditional life insurance products like Whole Life and Indexed Universal offer a steadfast promise of low to zero volatility, securing your funds against market fluctuations.

- Cash Value Accumulation: As your policy matures, it builds a notable cash value, presenting you with a goldmine of financial opportunities for your retirement income.

- Loan Interest Strategies: Imagine borrowing against your policy’s cash value; the interest you pay can be significantly outweighed by the annual retirement income surge, bestowing you with a lucrative arbitrage scenario.

-

Consider dividends—these incremental payouts can contribute to dividend growth over time, bolstering your policy’s cash value. Consistently rising dividends lead to heightened yields, aiding in covering your living expenses through a stable, reinforced income stream.

Remember, life insurance is not a spur-of-the-moment switch but a strategic move for sustained prosperity. By leveraging these policies adeptly, you position yourself to reap amplified financial benefits far into the future.

Stabilizing Your Financial Future with Life Insurance Asset Transfer

When approaching retirement, stabilizing your finances against market fluctuations can be a top priority. By reallocating a portion of your assets into a whole life insurance policy, you could potentially secure a more predictable source of income for your golden years.

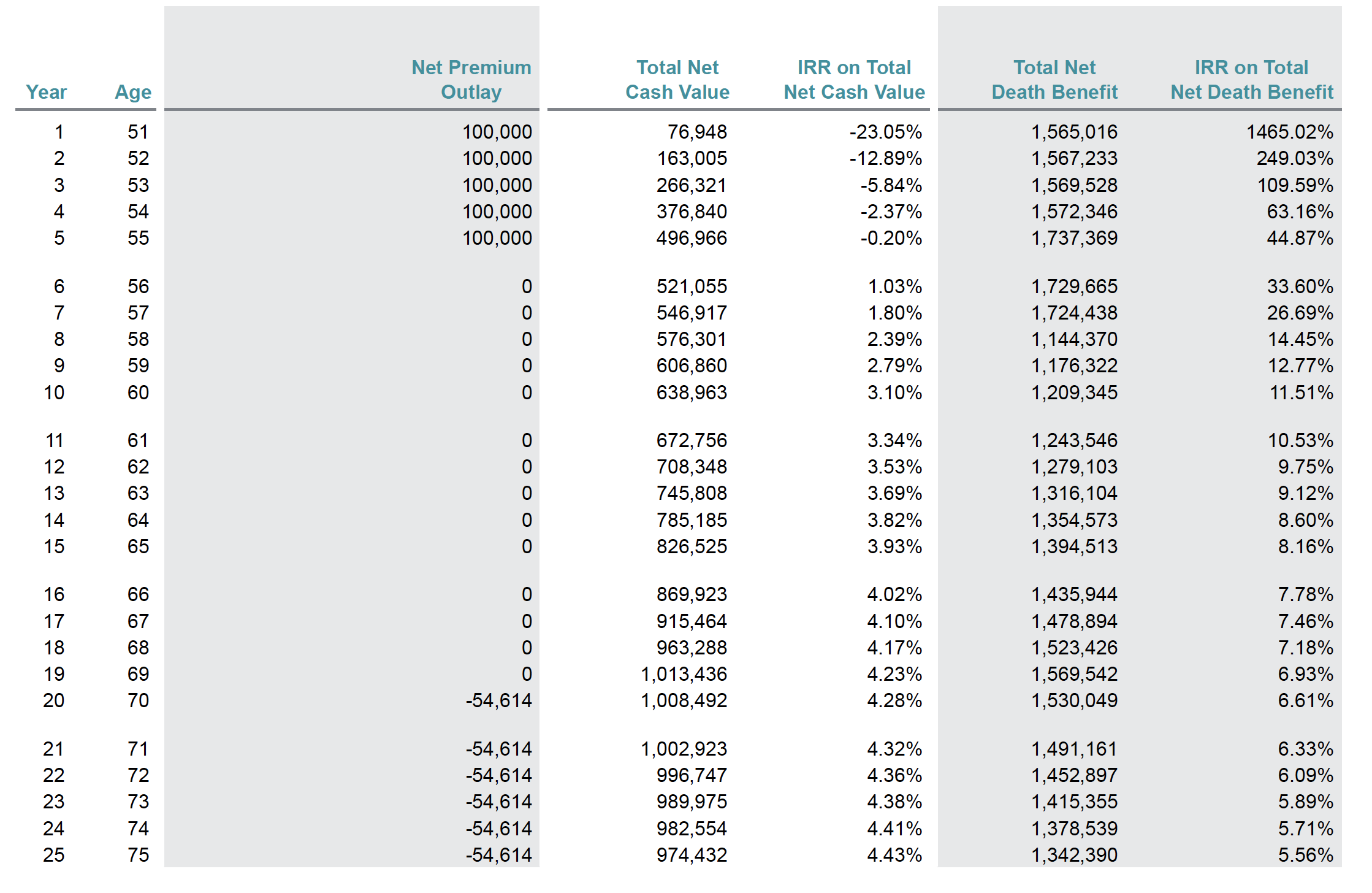

Imagine you’re a 50-year-old individual who has diligently amassed a notable asset base in preparation for retirement. Despite this, the possibility of market downturns affecting the value of your portfolio is a valid concern.

One tactic for safeguarding your financial future is to transfer $500,000 of your assets into a whole life insurance policy which is structured to maximize cash value growth over a death benefit. This transfer acts as a buffer by providing an asset that does not suffer from market volatility, ensuring the cash value of your policy will not depreciate.

| Years | Cash Value Growth | Income Potential |

|---|---|---|

| 10 | 3.10% Return | Substantial Increase |

| 20 | 4.28% Return | Much Higher than 4% |

The above table showcases the attractive returns one might expect over time with such a strategy. After two decades, it’s feasible to generate income close to a 5.5% annual distribution rate from this policy’s balance—completely tax-free and with no forced withdrawal schedule.

This lack of negative returns markedly enhances your withdrawal capacity when compared to the typical 4% safe withdrawal rate often associated with retirement planning. Essentially, while the rate of accumulation may fluctuate, the absence of downside risk with the policy amplifies your ability to sustain higher withdrawal rates.

If you opt to utilize policy loans for income, keeping up with the loan interest could meaningfully increase the annual income you extract from the policy. The arbitrage between the higher withdrawal rate and the loan interest could boost your disposable income, proving beneficial during retirement.

Meanwhile, your remaining assets, assuming they are invested in an equity-heavy portfolio, continue to carry the potential for standard stock market growth rates, providing a balanced mix of growth and stability for your overall asset allocation. This strategy isn’t rigid; it scales with your asset base, whether you have more to allocate or less.

Preparing Your Portfolio for Future Financial Stability

Consider that you’re 40 and contemplating the risks that may arise as you edge closer to retirement. Your savings are substantial, and you wonder if fine-tuning your strategy could proactively mitigate future risks.

Your preference is to keep your assets invested in the market to capitalize on potential growth over the next few decades.

Imagine channeling $50,000 from your annual savings into a whole life insurance policy. Traditionally, you might expect a certain outcome from such a strategy, projected to provide a solid retirement income.

However, enhancing this by coordinating with your other assets can be even more beneficial.

Whole life insurance policies come with an assumption of consistent dividends and are often coupled with the concept of taking a loan for income requirements, projected until a set age, like 100.

Typically, the loan accumulates interest, which isn’t paid out-of-pocket but added to the loan balance.

Alternatively, you might consider paying that loan interest yourself using funds from other assets.

By doing so, you exchange a portion of your relatively riskier assets for an interest repayment into your whole life insurance policy. This move could potentially skyrocket your annual income due to the policy, producing stable, non-taxable income.

Let’s break it down:

| Years | Loan Interest Paid | Income Gained |

|---|---|---|

| 1-5 | $79,246 | $459,115 |

This exchange reflects a significant income boost—almost $92,000 yearly—by offsetting some market risks through your whole life insurance.

You’d need to ensure that the income you forgo by reallocating assets to cover the loan interest meets or exceeds what you’d make if they remained invested elsewhere.

Whole life insurance stands out for its low volatility, offering a robust income generation feature compared to more fluctuating assets.

And when considering life insurance income, remember it’s already adjusted for taxes and fees.

Even if you stop relocating funds to cover life insurance loan interests in the future, you could still accumulate more income than projected initially.

Finding the perfect balance of asset allocation into life insurance as you age is complex, but it’s not about precision. It’s about understanding the opportunities at your disposal when integrating life insurance into your financial plan and its profound role in minimizing risk.

Incorporating life insurance into your investment mix can open up a myriad of options, presenting a potent means to decrease financial exposure.

While the topic is extensive, the possibilities life insurance brings to the table warrant further exploration on another occasion.