What is Gap insurance

What Is Gap Insurance?

In this article, we at the Guides Auto Team will explain everything you need to know about gap insurance and recommend the best car insurance companies for gap coverage.

If you’re shopping for auto coverage, the best way to find the lowest rates is to compare multiple car insurance quotes.

What Does Gap Insurance Cover?

If your financed car is totaled, gap insurance can cover the remaining amount on your loan should you owe more than the car is worth.

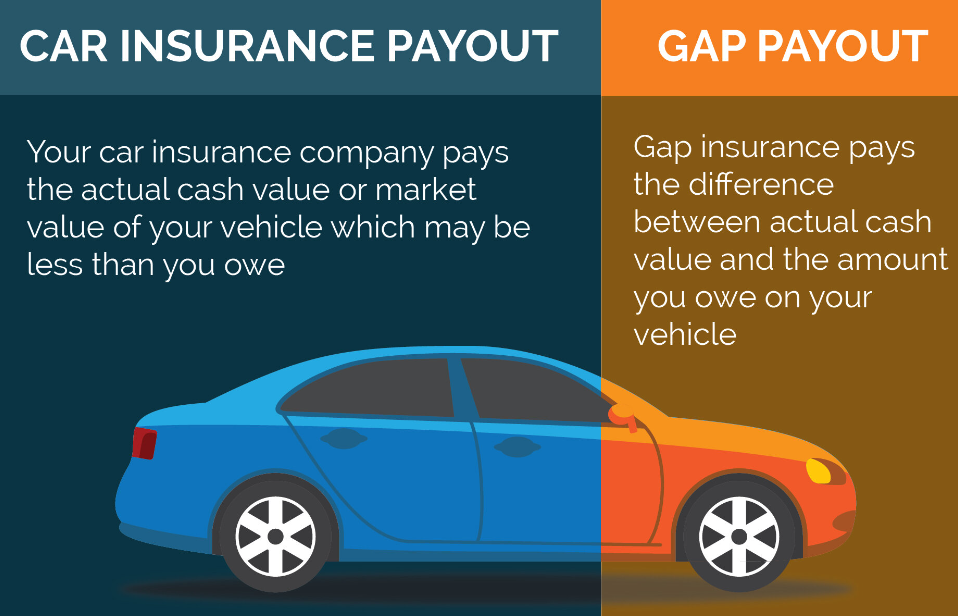

Gap insurance comes into play if your vehicle is financed and you make a total loss claim — either after your vehicle is totaled (the cost of the repairs would be more than the car is worth) or if it is stolen. When you submit a total loss claim, your insurer will pay a maximum of the actual cash value of your vehicle (ACV).

In some cases, the amount you still owe in car payments can exceed your car’s ACV. This is known as having negative equity or being upside down on your loan. Gap insurance, also sometimes called loan/lease payoff insurance, helps you pay off the loan in this situation. Remember, the loan doesn’t go away just because your car is totaled.

How Does Gap Insurance Work?

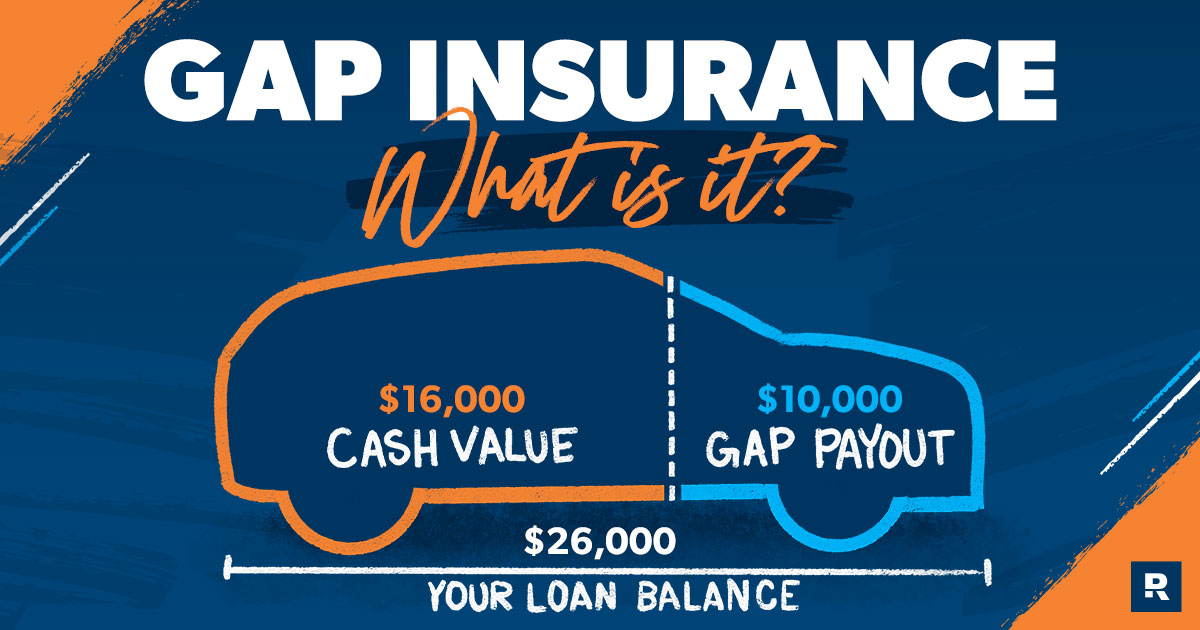

Consider the following example: Your vehicle is financed and you still owe $10,000 to your lender. You are involved in an accident, and the car is declared a total loss. The insurance claims adjuster determines that your car’s ACV is $8,000, and your insurer issues a check for this amount. Gap insurance covers the remaining $2,000 to pay off your auto loan balance.

As soon as you drive a new car off the lot, its value starts depreciating. If your new car is totaled within the first few years, you could owe the bank more than what your car is worth. Guaranteed asset protection, or “gap” insurance, covers this difference.

Do You Need Gap Insurance Coverage?

If your vehicle is not financed, there is no reason to purchase gap coverage. If you do finance your vehicle, gap coverage can be a good idea, but it depends on how much you drive and how quickly your car depreciates.

Keep in mind that cars can depreciate rapidly. According to the Insurance Information Institute, many vehicles depreciate 20% or more within the first year of ownership. If you don’t make a large down payment on your car, the amount you owe in car payments can quickly exceed your car’s value.

Is Gap Insurance Worth It?

If you are not financing or leasing your car, there is no reason to purchase gap insurance. But gap coverage can be worth it in a few situations. You should consider gap insurance coverage if:

- You made a small down payment

- You have a long finance period

- You drive a lot

- You purchased a vehicle that depreciates quickly

To calculate the potential value of gap insurance for yourself:

- Use Kelley Blue Book to estimate your car’s value. You may want to also estimate what your car’s value will be after each year of ownership until your car loan is fully paid.

- Review your loan terms. Check how much you will still owe in payments after each year of ownership and compare this against your car’s estimated value at that time.

- Calculate how much you will pay in gap coverage during those years.

- Compare your results. The difference between your car’s value and the amount you will owe in payments is the amount that gap coverage protects you from potentially having to pay.

In general, most new car buyers typically benefit from gap coverage while the vehicle is less than three model years old.

How Much Does Gap Insurance Cost?

The cost of gap insurance can vary but is usually inexpensive. If you buy gap insurance from the dealership, it can cost hundreds of dollars a year. If you add gap coverage to a car insurance policy that already includes collision and comprehensive insurance, it typically increases your premium by around $40 to $60 per year.

How Is Gap Insurance Calculated?

Lenders and dealers calculate what you pay for gap insurance based on your loan and your vehicle’s expected depreciation. Gap insurance can be more expensive for larger loans. Car insurance companies calculate your gap insurance cost based on your vehicle and your driving profile.

Does Gap Coverage Always Pay Out?

Gap insurance only pays out if the total loss claim is approved and the settlement you receive for your vehicle doesn’t cover your outstanding loan amount. If another driver was at fault, gap insurance can cover the difference between their insurance company’s settlement offer and the outstanding loan, as well.

When Does Gap Insurance Not Pay?

Some gap insurance policies limit the total amount you can receive. For example, Progressive’s gap insurance policy covers up to 25% of the vehicle’s ACV. It’s possible this gap payout wouldn’t cover the whole loan if your car had depreciated significantly.

Gap insurance wouldn’t pay out if your car was damaged but it wasn’t declared a total loss. Also, the insurance company can decline payments if you haven’t paid your own insurance premium.

Where To Buy Gap Insurance

You can get gap insurance from most major car insurance companies, though not all offer it. You can also get gap coverage from your dealership or auto lender when you purchase the vehicle. However, you’ll pay slightly more this way because the cost is added to your auto loan payments with interest.

Be aware that insurance companies only sell gap coverage as an add-on to an existing policy. In other words, you can’t have a Progressive policy and get State Farm gap insurance. You need to stick with the same provider you have.

Gap Coverage: Conclusion

Gap insurance can come in handy when you buy a new car to cover the difference between its value and what you owe on the loan in the case of a total loss. If your lender requires it, check if you can get it from your insurance company before using the dealer.

Auto Gap Insurance Companies: Recommended Providers

You can buy gap coverage from the car dealership, but it’s typically cheaper to add coverage to an existing policy. Find out what your own rates might be by reaching out for no-obligation quotes from top insurers.

USAA: 9.5 out of 10.0

We rate USAA highly because of its stellar customer service reputation and low rates. USAA policies are often the cheapest car insurance option for most drivers, partly because of the company’s discount offers, which include:

- Family discount

- Military installation discount

- Loyalty discount

- Safe driving discount

- Defensive driving discount

- Driver training discount

- New vehicle discount

- Multi-vehicle discount

- Low mileage discount

- Vehicle storage discount

- Good student discount

Unfortunately, USAA insurance is not available for everyone. To be eligible for a policy with USAA, you must be a military member or have a family member who has a USAA account.

USAA offers gap coverage as well as auto replacement assistance. Like gap coverage, auto replacement assistance kicks in after your vehicle has been totaled. This car insurance coverage will help to pay for the cost of a replacement vehicle that is similar to or newer than your wrecked vehicle.

Read more: USAA insurance review

Progressive: 9.2 out of 10.0

Progressive is a good choice for high-risk drivers, including those under 21, over 65 or who have a DUI/DWI on record. Like USAA, Progressive offers a number of car insurance discounts including:

- Multi-policy discount

- Multi-car discount

- Teen driver discount

- Good student discount

- Distant student discount

- Paperless billing discount

- Pay-in-full discount

- Homeowner discount

- Continuous coverage discount

- Online quote discount

Progressive offers loan/lease payoff coverage as a policy add-on. This covers up to 25% of your vehicle’s actual cash value. On average, this coverage costs $5 a month with Progressive.

Read more: Progressive insurance review

Gap Coverage Insurance: FAQ

Below are some common frequently asked questions about GAP insurance:

“Gap” stands for guaranteed asset protection. This type of insurance coverage pays the difference between your vehicle’s cash value and the amount you still owe in car payments in the event of a total loss claim (such as if your vehicle is totaled or stolen).

Gap insurance is something you purchase in addition to a full coverage policy. Full coverage usually encompasses liability insurance, collision insurance and comprehensive insurance. You may want gap insurance if your vehicle is financed, especially if you only made a small down payment when you purchased your car.

If your vehicle is totaled, your insurance provider will pay out a maximum of your car’s actual cash value. ACV is an estimate of the car’s retail value on the open market. If your vehicle is financed, you may owe more in payments than the total value of your car. If this happens, gap insurance coverage will make up the difference.

You may not be able to buy gap insurance at any time. Older vehicles are typically not eligible for gap insurance coverage. Specific requirements vary by insurer, but usually, any vehicle more than three model years old is not eligible for gap insurance coverage.

Several national auto insurers offer gap insurance, including:

- AAA

- Allstate

- Farmers

- Nationwide

- Progressive

- State Farm

- USAA

Geico does not offer gap insurance at this time. Your lender may still require you to have it, so you’ll get gap coverage options through the dealer when you purchase your vehicle.

Gap insurance does not cover theft. It only pays when your vehicle is totaled and you owe money on the loan. However, comprehensive insurance does cover theft, and lenders require comprehensive coverage on cars with auto loans.

You only need gap insurance until the remainder of your loan drops below the value of the vehicle. This is typically in the first couple of years of the loan. You can request that your car insurance company drops coverage at this point. However, if you financed gap insurance through a dealer, you’ll pay for it for the remainder of the loan unless you refinance.

Our Methodology

Because consumers rely on us to provide objective and accurate information, we created a comprehensive rating system to formulate our rankings of the best car insurance companies. We collected data on dozens of auto insurance providers to grade the companies on a wide range of ranking factors. The end result was an overall rating for each provider, with the insurers that scored the most points topping the list.

Here are the factors our ratings take into account:

- Cost (30% of total score): Auto insurance rate estimates generated by Quadrant Information Services and discount opportunities were both taken into consideration.

- Coverage (30% of total score): Companies that offer a variety of choices for insurance coverage are more likely to meet consumer needs.

- Reputation (15% of total score): Our research team considered market share, ratings from industry experts and years in business when giving this score.

- Availability (10% of total score): Auto insurance companies with greater state availability and few eligibility requirements scored highest in this category.

- Customer Experience (15% of total score): This score is based on volume of complaints reported by the NAIC and customer satisfaction ratings reported by J.D. Power. We also considered the responsiveness, friendliness and helpfulness of each insurance company’s customer service team based on our own shopper analysis.

*Data accurate at time of publication.